Is your Dream House Just a Dream - New Lending Rules

Canada's first-time home buyers may have to shelve their dream house fantasies due to lending changes many mortgage brokers say, the size of the mortgage many buyers qualify for will now be less.

Ottawa moved last week to tighten mortgage lending rules that will limit the amount many Canadians can borrow to help ensure that when interest rates rise, they'll still be able to make their payments.

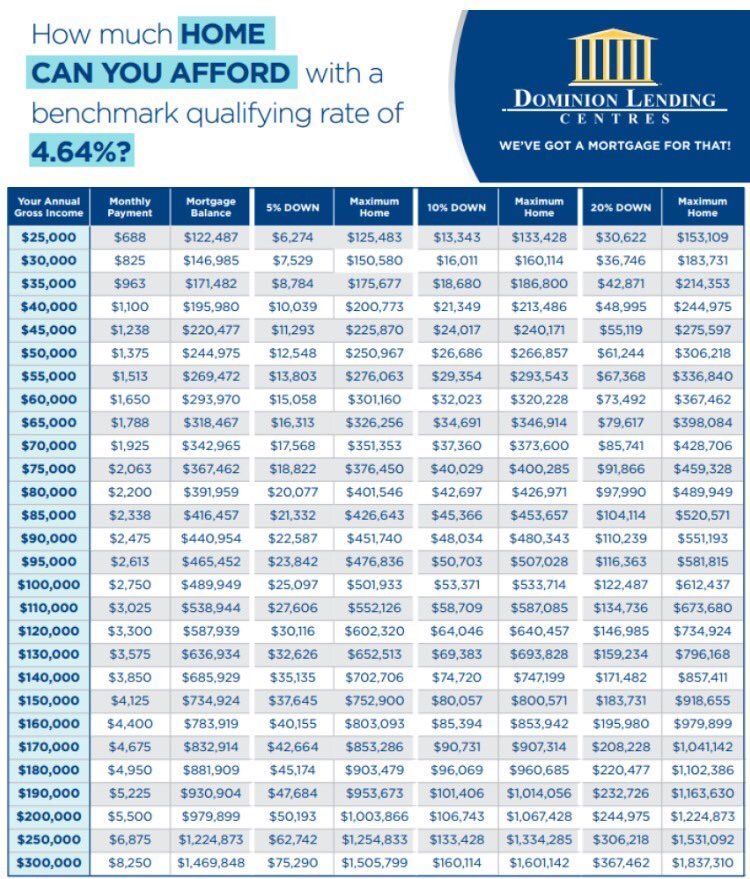

Under the new rules, a stress test that had only applied to borrowers who opted for variable rate mortgages or fixed rate mortgages with terms less than five years will now be used for all home buyers with less than a 20 per cent down payment. That means borrowers must be able to qualify for their mortgage using a higher interest rate than they will actually be paying on their mortgage. "You're not paying more, but you're going to be able to buy less house," Napolitano said.

The idea is that potential home buyers must be able to show that if interest rates were much higher than they are today, they'd still be able to make their mortgage payments and other costs related to home ownership.

It won't be uncommon for nervous lenders to turn down borrowers who just barely qualify or require a co-signer or a larger down payment. People who have less than 20 per cent down are going to qualify for a whole lot less money

The changes may mean that you will have to settle for a less expensive property, save for a larger down payment or wait until they are earning more.